PhilHealth Contribution 2026: Rates, Table, Computation & How to Pay

PhilHealth contribution rates, the full table, and how to pay — all updated for 2026. See exactly how much you owe, how to compute it, and what the new interest waiver means for unpaid balances.

A PhilHealth contribution is the monthly premium that funds your coverage under the National Health Insurance Program, and as of 2026, the rate remains a flat 5% of your monthly basic salary or declared income. This guide breaks down exactly how much you need to pay across employed, self-employed, voluntary, and OFW categories, how to compute it yourself, where to pay, how to check your record online, and what to do if you have missed payments, including the new 2026 interest waiver program.

What Is a PhilHealth Contribution?

A PhilHealth contribution, sometimes shown on payslips as an EE NHIP contribution (short for “employee” and “National Health Insurance Program”), is the regular premium paid into the National Health Insurance Fund. PhilHealth pools these contributions and uses them to pay part of a member’s hospital and outpatient bills once they get sick, get confined, or need covered medical services. Your contribution amount is based on your monthly basic salary or declared income, not on your age, health condition, or family size, and the same percentage rate applies to healthy members and those already managing a medical condition alike. The deduction you see labeled “PhilHealth” or “PHIC” on your payslip is simply your half of this premium, with your employer covering the other half.

Who Is Required to Pay PhilHealth Contributions?

Contribution requirements differ slightly depending on your membership category, so it helps to know where you fall before checking the rates below.

Employed Members

Anyone with an employer-employee relationship, whether in government or private companies, pays through automatic payroll deduction.

Self-Employed and Informal Economy Workers

Freelancers, online sellers, tricycle drivers, and other self-earning individuals register and pay their own full contribution based on declared income.

Voluntary Members

Anyone without a regular employer, including those temporarily out of work, registers and pays voluntarily to keep coverage active.

OFWs

Land-based and sea-based overseas workers are mandatory contributors, usually paying annually or semi-annually before deployment.

Kasambahay

Household employers shoulder the full premium for helpers earning below ₱5,000 monthly; above that threshold, the standard 50-50 split applies.

Senior citizens, indigents, and sponsored members

These groups are fully subsidized and pay no premium at all.

If you do not belong to a subsidized category and currently have no employer, you are still expected to register and contribute as a voluntary member to keep your PhilHealth membership active.

PhilHealth Contribution Rate and Table for 2026

The PhilHealth contribution rate has stayed flat at 5% since 2024, and there is no scheduled increase for 2026. This rate applies to all direct contributors, with the exact peso amount depending on income and membership type.

Employed Members

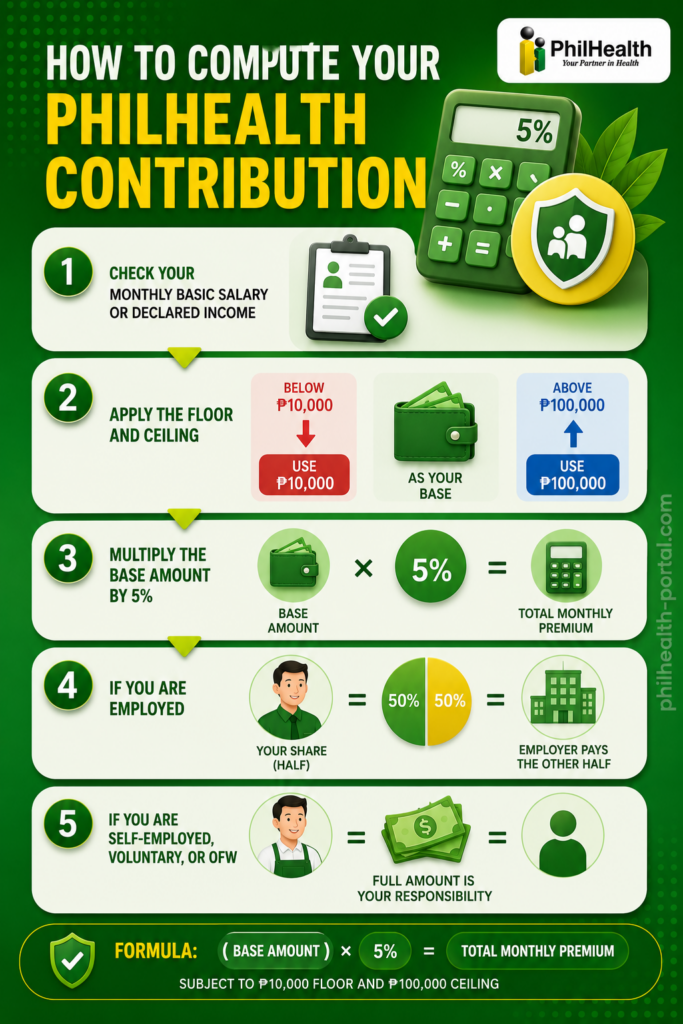

Employed members split the 5% premium equally with their employer, paying 2.5% each. The income floor is ₱10,000 and the ceiling is ₱100,000, which sets the minimum and maximum monthly contribution regardless of how high a salary goes beyond that ceiling.

| Monthly Basic Salary | Total Monthly Premium (5%) | Employee Share | Employer Share |

|---|---|---|---|

| ₱10,000 and below | ₱500.00 | ₱250.00 | ₱250.00 |

| ₱15,000 | ₱750.00 | ₱375.00 | ₱375.00 |

| ₱25,000 | ₱1,250.00 | ₱625.00 | ₱625.00 |

| ₱40,000 | ₱2,000.00 | ₱1,000.00 | ₱1,000.00 |

| ₱60,000 | ₱3,000.00 | ₱1,500.00 | ₱1,500.00 |

| ₱100,000 and above | ₱5,000.00 | ₱2,500.00 | ₱2,500.00 |

Self-Employed, Voluntary Members & OFWs

How much is the PhilHealth contribution for voluntary members? The same 5% rate applies, but since there is no employer to share the cost, self-employed individuals, voluntary members, and OFWs pay the full amount themselves based on declared monthly income.

| Declared Monthly Income | Total Monthly Premium (5%) |

|---|---|

| ₱10,000 and below | ₱500.00 |

| ₱20,000 | ₱1,000.00 |

| ₱35,000 | ₱1,750.00 |

| ₱50,000 | ₱2,500.00 |

| ₱100,000 and above | ₱5,000.00 |

OFWs can pay this amount monthly, quarterly, semi-annually, or annually, whichever fits their work schedule abroad. Self-employed members typically declare their income using their latest Income Tax Return or a notarized affidavit of income if they do not yet file one.

Kasambahay, Senior Citizens & Indigent Members

Household employers cover the full premium for a Kasambahay earning under ₱5,000 a month and cannot deduct any amount from that worker’s pay. Once a Kasambahay’s salary reaches ₱5,000 or more, the standard employer-employee split applies just like any other formal employee. Senior citizens, identified indigents, sponsored members, and registered PWDs are exempt from paying any premium, since the national or local government shoulders their coverage in full.

How to Compute Your PhilHealth Contribution

The basic PhilHealth contribution formula is straightforward: multiply your monthly basic salary or declared income by 5%, applying the ₱10,000 floor and ₱100,000 ceiling first if your income falls outside that range.

For example, an employee earning ₱30,000 a month pays a total premium of ₱1,500, split into ₱750 from the employee and ₱750 from the employer. A voluntary member declaring the same ₱30,000 income pays the full ₱1,500 on their own, since there is no employer contribution to offset the cost.

PhilHealth Contribution Table: Past Years (2019–2025)

If you are settling old contributions, applying for a loan, or simply checking what you paid in a previous year, here is how the PhilHealth contribution rate progressed under the Universal Health Care Act.

| Year | Premium Rate | Income Ceiling | Maximum Monthly Premium |

|---|---|---|---|

| 2019 | 2.75% | ₱40,000 | ₱1,100 |

| 2020 | 3.00% | ₱60,000 | ₱1,800 |

| 2021 | 3.50% | ₱70,000 | ₱2,450 |

| 2022 | 4.00% | ₱80,000 | ₱3,200 |

| 2023 | 4.00%* | ₱80,000 | ₱3,200 |

| 2024 | 5.00% | ₱100,000 | ₱5,000 |

| 2025 | 5.00% | ₱100,000 | ₱5,000 |

| 2026 | 5.00% | ₱100,000 | ₱5,000 |

*The scheduled increase to 4.5% for 2023 was suspended by presidential order, so members continued paying the 2022 rate that year. The income floor stayed at ₱10,000 across every year shown above.

How to Pay PhilHealth Contributions

Employed members generally do not pay PhilHealth directly, since contributions come out of payroll and employers remit them through the Electronic Premium Remittance System, or EPRS. Self-employed, voluntary, and OFW members, however, need to pay their own contributions, and the process now requires an extra step that many members are not yet used to. You can also Pay PhilHealth Online and that is the easiest way.

Since April 2026, PhilHealth enforces a “No SPA, No Payment” policy for self-paying members. You must generate a Statement of Premium Account, or SPA, through the Member Portal before any payment channel will accept your transaction. The SPA locks in your exact coverage period and amount due, producing a reference number that payment platforms use to post your contribution correctly.

Once you have a valid SPA, you can pay through:

- GCash or Maya – Open the Bills or Government section, select PhilHealth, and enter your SPA reference and PIN.

- Online banking apps – Several partner banks accept PhilHealth payments directly using the SPA reference.

- Bayad Center and accredited collecting agents – Present your SPA and PIN over the counter for manual processing.

- PhilHealth branch – Pay in person at any LHIO if you prefer a face-to-face transaction.

PhilHealth Employers, meanwhile, generate a separate SPA for the company through EPRS after submitting their Premium Remittance Form, then settle the total amount through partner banks or accredited collection channels. Payments typically post within one to five working days, so paying a few days before your deadline avoids any last-minute posting delays.

How to Check Your PhilHealth Contribution Online

To check your PhilHealth contribution status, log in to the Member Portal using your 12-digit PIN and password, then open the “Premium Contributions” or “Print MDR” section of your dashboard. Your Member Data Record lists every posted contribution by month, which lets you confirm whether your employer’s remittances or your own payments are reflecting correctly. If a recent payment is missing, check the date against the one-to-five working day posting window before assuming something went wrong, since contributions made within the past few days may simply still be processing.

How to Get a PhilHealth Certificate of Contribution

A Certificate of Contribution, sometimes called a Certificate of Premium Payment, is an official document confirming how much you have paid into PhilHealth over a given period. Members typically request this for loan applications, scholarship requirements, visa processing, or audits where proof of consistent contributions is needed. You can request it online by sending your full name, PIN, and the period you need covered to the PhilHealth Action Center, or by visiting any LHIO directly with a valid ID and a written request. Processing usually takes a few working days, so it is best to request the certificate well ahead of any submission deadline.

What Happens If You Miss a PhilHealth Contribution? (Penalties and the 2026 Interest Waiver)

Missing a contribution does not cancel your membership outright, but it can affect your benefit eligibility if your payment record falls behind the required number of months for certain claims. For employers specifically, unpaid or late-remitted contributions accrue 3% interest per month, compounded, which can balloon quickly if left unpaid for an extended period.

In January 2026, following a directive from President Marcos, PhilHealth rolled out a one-time interest waiver program covering missed contributions from July 2013 to December 2024. This waiver applies only to the interest charges, not the unpaid principal contributions themselves, and runs on a graduated scale: employers who settle their full balance within one month qualify for a complete waiver of interest, those settling within two to six months pay a reduced 1% interest, and those taking seven to twelve months pay 2% interest. The settlement window runs through December 31, 2026, and employers availing of the waiver must register (also can Register Online) their employees under the YAKAP program and complete the First Patient Encounter requirement to qualify. Guidelines for self-employed members are being released separately, so it is worth checking PhilHealth’s official advisories if you fall under that category with unpaid voluntary contributions.

What Your Contribution Pays For

Your monthly premium funds both inpatient and outpatient benefits delivered through PhilHealth’s accredited network. Inpatient coverage uses fixed case rates, where PhilHealth pays a set amount per diagnosis directly to the hospital, while catastrophic and high-cost conditions such as certain cancers, kidney transplants, and major cardiovascular procedures fall under the Z Benefits packages, which provide more substantial support given how expensive these treatments are. Outpatient and primary care benefits run through the YAKAP program, offering free consultations, selected lab tests, cancer screenings, and up to ₱20,000 a year in essential medicines once a member completes clinic empanelment. Maternity care, dialysis, TB-DOTS treatment, and HIV/AIDS packages round out the major benefit categories your contributions help sustain.

Common Mistakes to Avoid

A surprising number of payment issues trace back to a handful of avoidable mistakes. Paying without first generating a fresh SPA is now the most common error among self-paying members, since an expired or reused SPA reference simply gets rejected by GCash, Maya, and partner banks. Declaring an outdated income bracket is another frequent issue for self-employed and voluntary members, particularly after a raise or a business income increase that was never reported to PhilHealth. Employers sometimes assume contributions are remitted automatically once deducted from payroll, when in fact a separate EPRS submission and payment step is still required every cycle. Finally, many members forget to verify their MDR after paying, missing posting delays or errors until they need to file a claim and discover a gap in their record.

Tips for Managing Your PhilHealth Contributions

Set a recurring reminder to generate your SPA and pay a few days before your deadline rather than on the exact due date, since posting can take up to five working days. Keep digital copies of your SPA, receipts, and MDR printouts in one folder so you can produce proof of payment quickly if a dispute or claim comes up. If you are self-employed or voluntary, review your declared income once a year and update it if it no longer matches your actual earnings, since this affects both your contribution amount and your benefit eligibility. Employers should reconcile their EPRS reports against payroll deductions every cycle to catch discrepancies early, well before they compound into the kind of interest charges the 2026 waiver program was designed to address.

Frequently Asked Questions

How much is the PhilHealth contribution in 2026?

The rate is a flat 5% of monthly basic salary or declared income, with a ₱500 minimum and ₱5,000 maximum monthly premium, split equally between employer and employee for formal-sector workers.

How much is the PhilHealth contribution for voluntary members?

Voluntary members pay the full 5% on their own, since there is no employer to share the cost, ranging from ₱500 to ₱5,000 a month depending on declared income.

How do I compute my PhilHealth contribution?

Multiply your monthly basic salary or declared income by 5%, applying the ₱10,000 floor and ₱100,000 ceiling if your income falls outside that range; employed members then split the result in half with their employer.

Where can I pay my PhilHealth contribution?

You can pay through GCash, Maya, partner banks, Bayad Center, or any PhilHealth branch, but self-paying members must first generate a Statement of Premium Account before any channel will accept the payment.

How do I check my PhilHealth contribution online?

Log in to the PhilHealth Member Portal with your PIN and password, then open the “Print MDR” or “Premium Contributions” section to view your posted payment history.

What happens if I miss a PhilHealth contribution?

Your membership stays active, but missed contributions can affect benefit eligibility and, for employers, accrue 3% monthly interest; the 2026 waiver program allows settling unpaid amounts from July 2013 to December 2024 with reduced or waived interest.

How do I get a PhilHealth certificate of contribution?

Request one through the PhilHealth Action Center by email or visit any LHIO with a valid ID, stating the period you need covered; processing typically takes a few working days.

Is PhilHealth contribution mandatory for the unemployed?

If you are not covered as an indigent, senior citizen, or dependent, you are expected to register and pay as a voluntary member to keep your coverage active while unemployed.

Conclusion

Understanding your PhilHealth contribution comes down to three things: knowing your correct rate and bracket, paying through the right channel with a valid SPA, and checking your MDR regularly to confirm everything posted correctly. The rate has held steady at 5% through 2026, which gives members a stable number to plan around, while the new interest waiver program offers a genuine opportunity for employers and self-employed individuals sitting on old unpaid balances to settle them without the usual compounding penalty. Staying current on your contributions, rather than catching up after the fact, remains the simplest way to keep your coverage and your family’s benefits fully intact.